¥1,700 trillion flowing into a ¥1,300 trillion market

When capital exceeds the entire market cap of the Tokyo Stock Exchange, opportunity lies in stock selection.

Executive Summary

For three decades following the 1989 bubble, Japanese households and corporations engaged in rational defensive hoarding. In a deflationary world, cash was the only hedge. This collective deleveraging created a massive liquidity vault—¥1,100 trillion in household deposits and ¥600 trillion in corporate reserves.

Today, macroeconomic and structural forces are forcing this capital back into motion. Inflation and negative real rates have broken down the multi-decade deflationary mindset. METI’s governance reforms and expanded NISA incentives are accelerating the flow of zero-yield savings into equities.

The ¥1,700 trillion vault is now open—and capital flow is just getting started.

With TOPIX trading at ~19.8x earnings, the broad index offers limited margin of safety.

The opportunity has migrated to individual stock selection.

Forces Driving Capital Reallocation

Macro catalysts put capital into motion → Structural reforms direct how capital flows → Corporate fundamentals dictate where capital flows end up.

The ongoing stress test—sticky inflation and a historically weak yen—has revealed where true value lies.

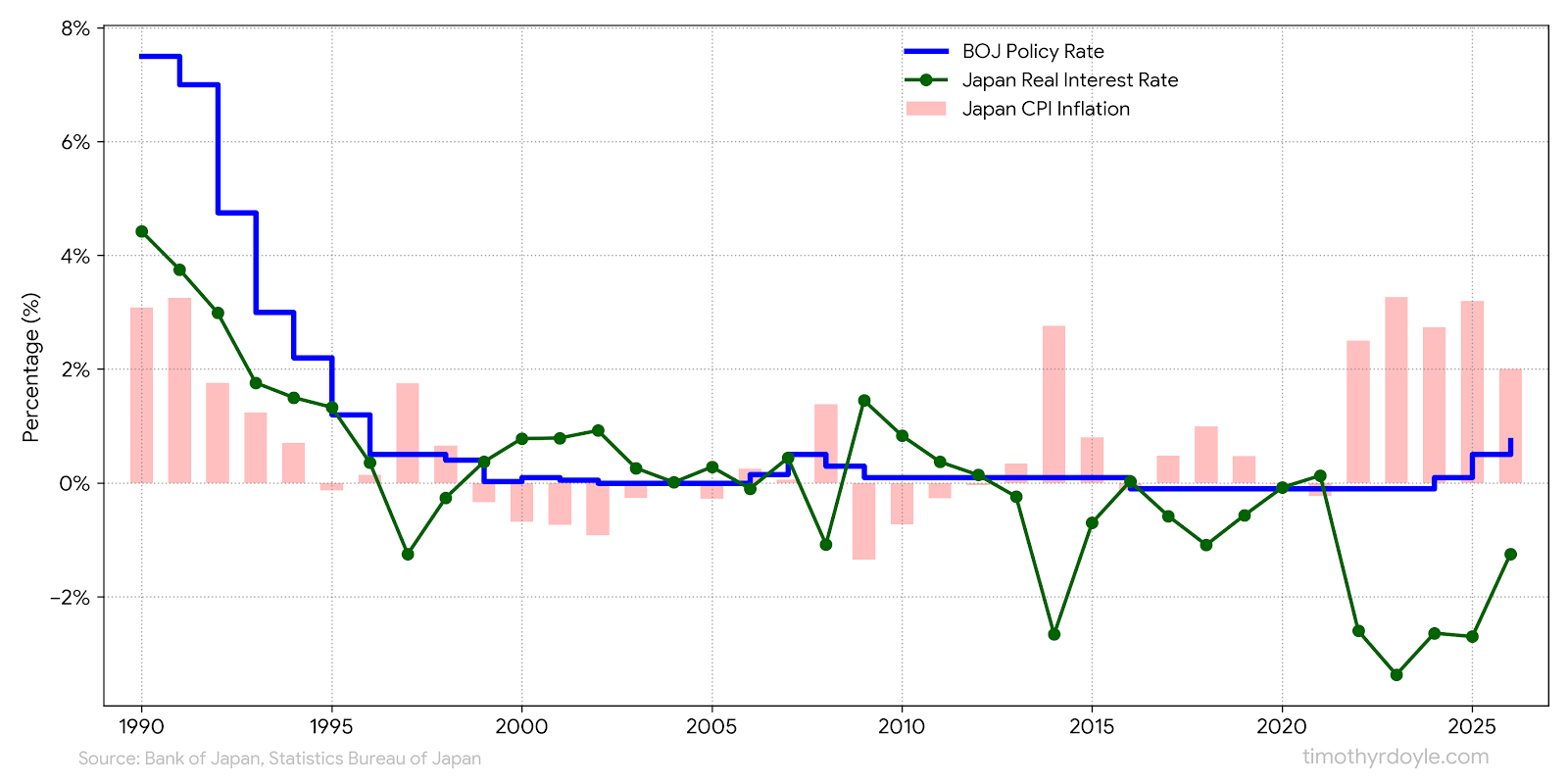

📉 Negative Real Rates: The Penalty on Cash

Key Insight: Japan’s real rates have been more negative than at any point since 1990. Cash holders are being systematically penalized—forcing capital into risk assets.

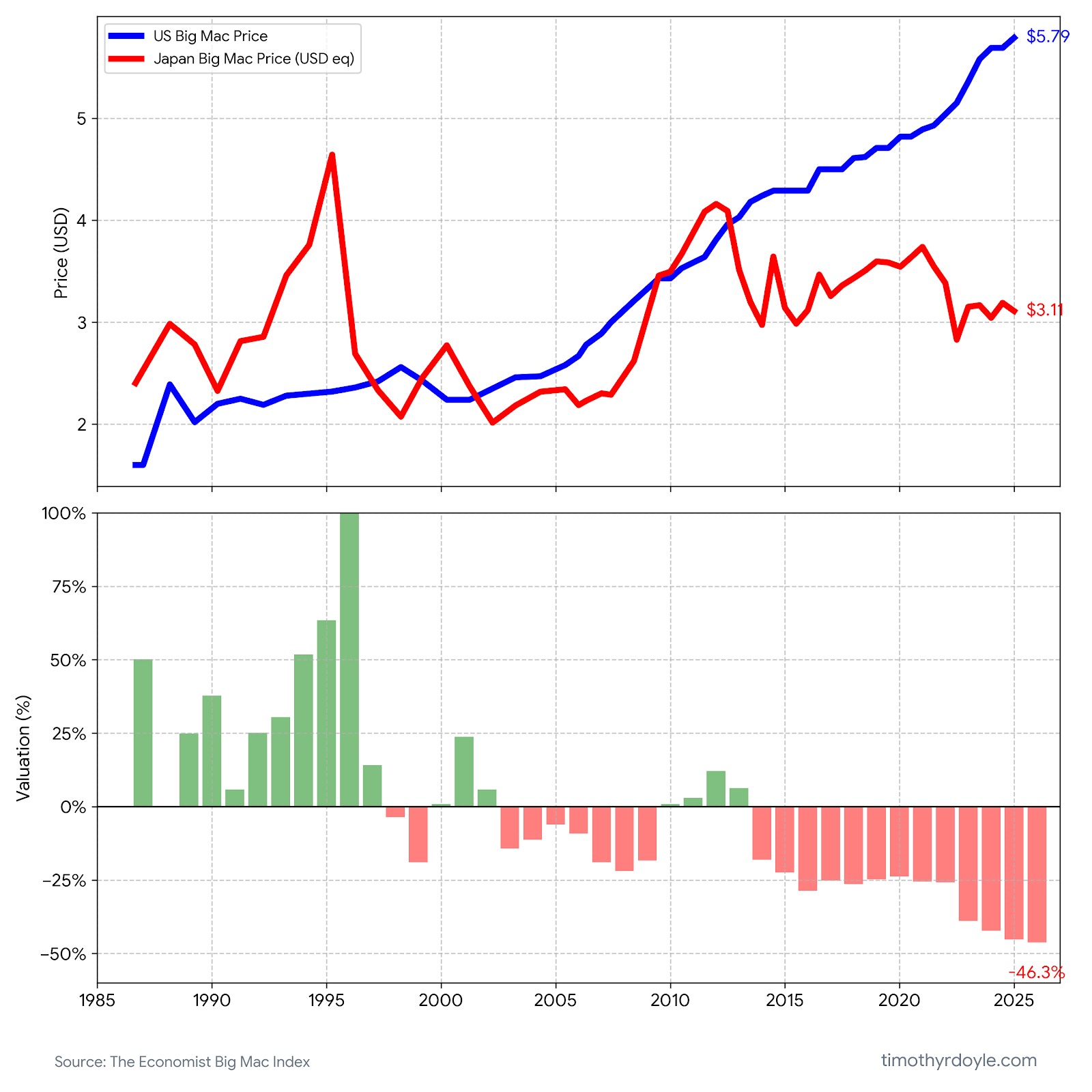

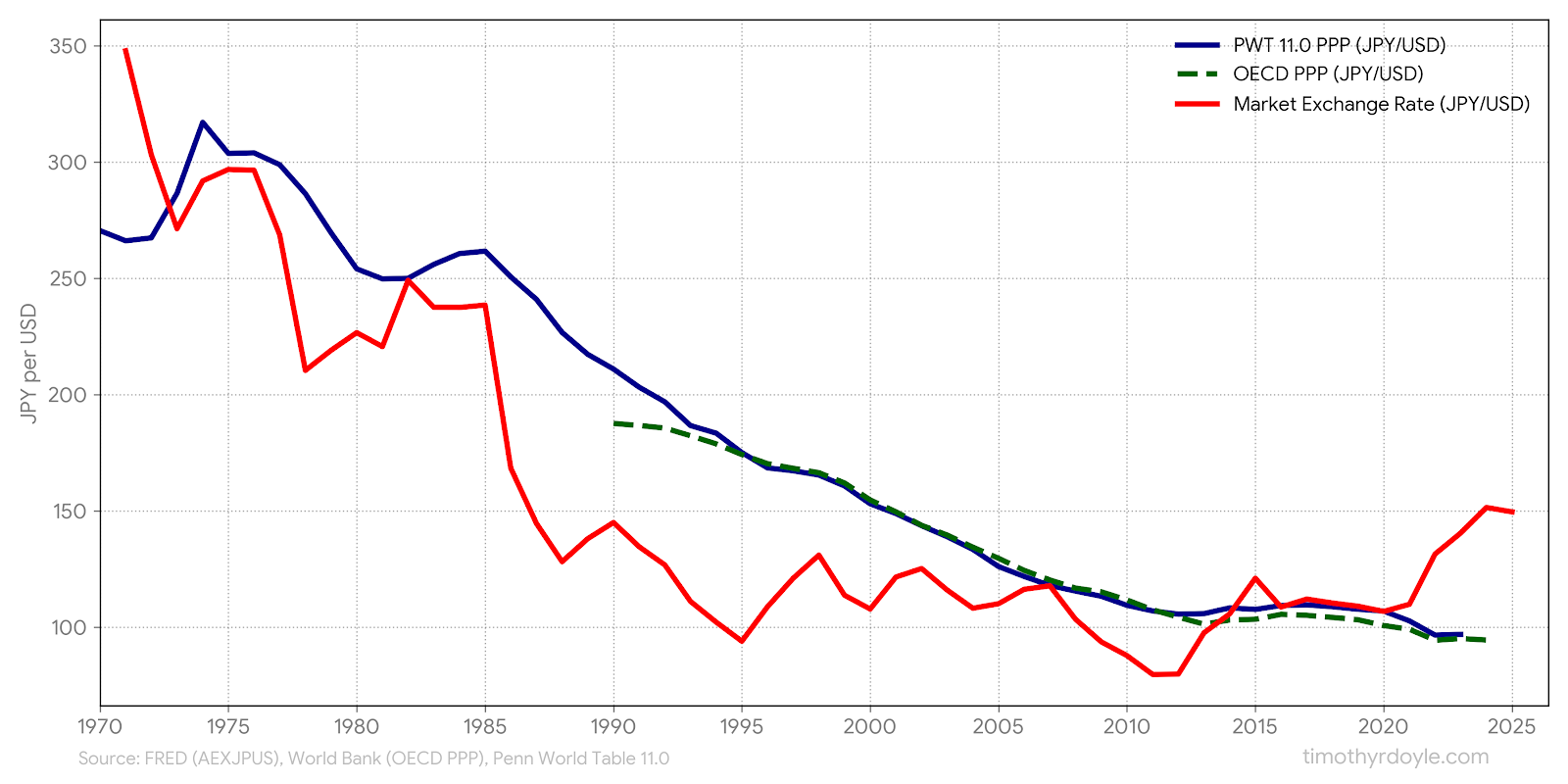

🍔 Extreme Yen Undervaluation: A Rare Structural Arbitrage

The Big Mac test: In an efficient market, a Big Mac in Tokyo should cost the same as one in New York. It doesn’t—and the gap is at multi-decade extremes.

The Embedded Call Option: Buying domestic Japanese stocks provides a free option on yen reversion. If currency mean-reverts, dollar investors capture equity appreciation PLUS the currency windfall.

⚖️ Government Coercion: METI Reforms & NISA Incentives

The Tokyo Stock Exchange’s “name and shame” regime is forcing capital efficiency. Companies trading below book value face delisting. Record ¥20 trillion in buybacks in 2025 prove the vault is open.

Three Sources of Asymmetric Upside

Macro catalysts and structural reforms are mobilizing ¥1,700 trillion into equities—but flow alone does not guarantee returns. The superior strategy targets domestic firms that have already proven their resilience during the weak yen stress test, providing limited downside on yen weakness persistence and/or interest rate volatility and significant upside should the yen strengthen:

🛡️ Weak Yen Moat

Dominant domestic firms using pricing power to gain volumes on sub-scale rivals struggling with import inflation

🏦 Interest Rate Hedge

Fortress balance sheets generating interest income that offsets valuation compression should rates rise significantly

📈 Free Call Option

If the yen normalizes, firms capture massive margin windfalls as input costs collapse while pricing remains sticky

Read the Full Paper

Deep dive into: Macro Catalysts • Structural Reform Incentives • Stock selection frameworks • Screening methodology • Risk mitigation strategies

📄 Read Full Paper (PDF, 29 pages)

Published March 2026

About the Author: Timothy R. Doyle is an independent thinker applying multidisciplinary frameworks to identify where consensus may drift from the underlying reality.